Market Risk

What is Market Risk?

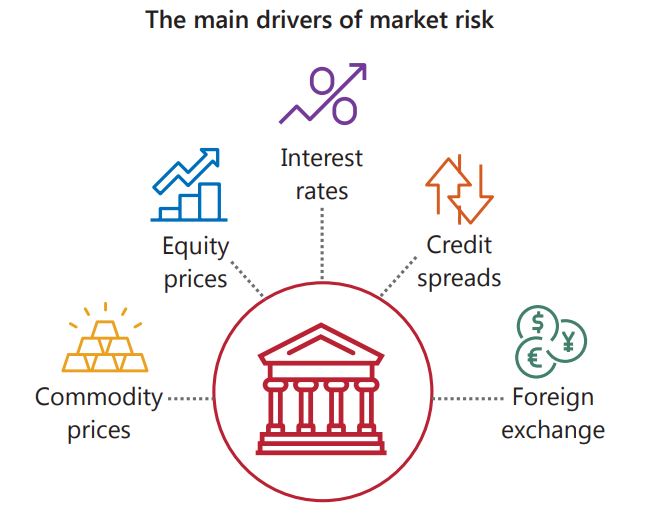

According to the Basel III framework, market risk is defined as the risk of losses arising from movements in market prices.

The market risk framework aims to ensure that banks maintain a minimum level of regulatory capital, to absorb losses arising from movements in market prices of instruments held in the trading book.

The risks subject to market risk capital requirements include but are not limited to:

(1) default risk, interest rate risk, credit spread risk, equity risk, foreign exchange (FX) risk and commodities risk for trading book instruments; and

(2) FX risk and commodities risk for banking book instruments.

All transactions, including forward sales and purchases, shall be included in the calculation of capital requirements as of the date on which they were entered into. Although regular reporting will in principle take place only at intervals (quarterly in most countries), banks are expected to manage their market risk in such a way that the capital requirements are being met on a continuous basis, including at the close of each business day.

Supervisory authorities have at their disposal a number of effective measures to ensure that banks do not window-dress by showing significantly lower market risk positions on reporting dates. Banks will also be expected to maintain strict risk management systems to ensure that intraday exposures are not excessive. If a bank fails to meet the capital requirements at any time, the national authority shall ensure that the bank takes immediate measures to rectify the situation.

A matched currency risk position will protect a bank against loss from movements in exchange rates, but will not necessarily protect its capital adequacy ratio. If a bank has its capital denominated in its domestic currency and has a portfolio of foreign currency assets and liabilities that is completely matched, its capital/asset ratio will fall if the domestic currency depreciates. By running a short risk position in the domestic currency, the bank can protect its capital adequacy ratio, although the risk position would lead to a loss if the domestic currency were to appreciate.

Learning from the Annual Reports

Market risk, important parts from the 2021 Annual Report, Barclays PLC Annual Report 2021

Market risk is the risk of loss arising from potential adverse changes in the value of the Group’s assets and liabilities from fluctuation in market variables including, but not limited to, interest rates, foreign exchange, equity prices, commodity prices, credit spreads, implied volatilities and asset correlations.

Overview

Market risk arises primarily as a result of client facilitation in wholesale markets, involving market-making activities, risk management solutions and execution of syndications. Upon execution of a trade with a client, the Group will look to hedge against the risk of the trade moving in an adverse direction. Mismatches between client transactions and hedges result in market risk due to changes in asset prices, volatility or correlations.

Organisation, roles and responsibilities

Market risk in the businesses resides primarily in Barclays International and Treasury. These businesses have the mandate to assume market risk. The front office and Treasury trading desks are responsible for managing market risk on a day-to-day basis, where they are required to understand and adhere to all limits applicable to their businesses. The Market Risk team supports the trading desks with the day-to-day limit management of market risk exposures through governance processes which are outlined in supporting market risk policies and standards. Market risk oversight and challenge is provided by business committees and Group committees, including the Market Risk Committee (MRC).

The objectives of market risk management are to:

■ identify, understand and control market risk by robust measurement, limit setting, reporting and oversight

■ facilitate business growth within a controlled and transparent risk management framework

■ control market risk in the businesses according to the allocated appetite. To meet the above objectives, a governance structure is in place to manage these risks consistent with the ERMF.

The BRC recommends market risk appetite to the Board for their approval. The Market Risk Principal Risk Lead (PR Lead) is responsible for the Market Risk Control Framework and, under delegated authority from the Group CRO, agrees with the business CROs a limit framework within the context of the approved market risk appetite.

The MRC reviews and makes recommendations concerning the group-wide market risk profile. This includes overseeing the operation of the Market Risk Framework and associated standards and policies; reviewing market or regulatory issues and limits and utilisation.

The committee is chaired by the PR Lead and attendees include the business heads of market risk and business aligned market risk managers. In addition to MRC, the Corporate and Investment Bank Risk Committee (‘CIBRC’) is the main forum in which market risk exposures are discussed and reviewed with senior business heads. The Committee is chaired by the CRO of Barclays International and meets weekly, covering current market events, notable market risk exposures, and key risk topics. New business initiatives are generally socialised at CIBRC before any changes to risk appetite or associated limits are considered in other governance committees.

The head of each business is accountable for all market risks associated with its activities, while the head of the market risk team covering each business is responsible for implementing the risk control framework for market risk.

Market risk, important parts from the 2021 Annual Report, Lloyds Banking Group plc

Market risk is defined as the risk that the Group's capital or earnings profile is affected by adverse market rates or prices, in particular interest rates and credit spreads in the Banking business, interest rates, equity prices and credit spreads in the Insurance business, and credit spreads in the Group’s defined benefit pension schemes.

The Group’s trading book assets and liabilities are originated within the Commercial Banking division. Within the Group’s balance sheet these fall under the trading assets and liabilities and derivative financial instruments.

Derivative assets and liabilities are held by the Group for three main purposes: to provide risk management solutions for clients, to manage portfolio risks arising from client business and to manage and hedge the Group’s own risks. Insurance business assets and liabilities relate to policyholder funds, as well as shareholder invested assets, including annuity funds. The Group recognises the value of in-force business in respect of Insurance’s long-term life assurance contracts as an asset in the balance sheet.

The Group ensures that it has adequate cash and balances at central banks and stocks of high quality liquid assets (e.g. gilts or US Treasury securities) that can be converted easily into cash to meet liquidity requirements. The majority of these assets are asset swapped and held at fair value through other comprehensive income.

The majority of debt issuance originates from the Group’s capital and funding activities and the interest rate risk of the debt issued is hedged by swapping them into a floating rate.

The non-trading book primarily consists of customer on-balance sheet activities and the Group’s capital and funding activities, which expose it to the risk of adverse movements in market rates or prices, predominantly interest rates, credit spreads, exchange rates and equity prices.

MEASUREMENT

Group risk appetite is calibrated primarily to a number of multi-risk Group economic scenarios, and is supplemented with sensitivity based measures. The scenarios assess the impact of unlikely, but plausible, adverse stresses on income with the worst case for banking activities, defined benefit pensions, insurance and trading portfolios reported against independently, and across the Group as a whole.

The Group risk appetite is cascaded first to the Group Asset and Liability Committee (GALCO), chaired by the Chief Financial Officer, where risk appetite is approved and monitored by risk type, and then to the Group Market Risk Committee (GMRC) where risk appetite is sub-allocated by division. These metrics are reviewed regularly by senior management to inform effective decision-making.

MITIGATION

GALCO is responsible for approving and monitoring Group market risks, management techniques, market risk measures, behavioural assumptions, and the market risk policy. Various mitigation activities are assessed and undertaken across the Group to manage portfolios and seek to ensure they remain within approved limits.

The mitigation actions will vary dependent on exposure but will, in general, look to reduce risk in a cost effective manner by offsetting balance sheet exposures and externalising to the financial markets dependent on market liquidity. The market risk policy is owned by Group Corporate Treasury (GCT) and refreshed annually. The policy is underpinned by supplementary market risk procedures, which define specific market risk management and oversight requirements.

MONITORING

GALCO and GMRC regularly review high level market risk exposure as part of the wider risk management framework. They also make recommendations to the Board concerning overall market risk appetite and market risk policy. Exposures at lower levels of delegation are monitored at various intervals according to their volatility, from daily in the case of trading portfolios to monthly or quarterly in the case of less volatile portfolios. Levels of exposures compared to approved limits and triggers are monitored by Risk and appropriate escalation procedures are in place.

How market risks arise and are managed across the Group’s activities is considered in more detail below.

BANKING ACTIVITIES

Exposures

The Group’s banking activities expose it to the risk of adverse movements in market rates or prices, predominantly interest rates, credit spreads, exchange rates and equity prices. The volatility of market rates or prices can be affected by both the transparency of prices and the amount of liquidity in the market for the relevant asset, liability or instrument.

Interest rate risk

Yield curve risk in the Group’s divisional portfolios, and in the Group’s capital and funding activities, arises from the different repricing characteristics of the Group’s non-trading assets, liabilities and off-balance sheet positions.

Basis risk arises from the potential changes in spreads between indices, for example where the Group lends with reference to a central bank rate but funds with reference to a market rate, e.g. SONIA, and the spread between these two rates widens or tightens. Optionality risk arises predominantly from embedded optionality within assets, liabilities or off-balance sheet items where either the Group or the customer can affect the size or timing of cash flows. One example of this is mortgage prepayment risk where the customer owns an option allowing them to prepay when it is economical to do so. This can result in customer balances amortising more quickly or slowly than anticipated due to customers’ response to changes in economic conditions.

Foreign exchange risk

Economic foreign exchange exposure arises from the Group’s investment in its overseas operations. In addition, the Group incurs foreign exchange risk through non-functional currency flows from services provided by customer-facing divisions, the Group’s debt and capital management programmes and is exposed to volatility in its CET1 ratio, due to the impact of changes in foreign exchange rates on the retranslation of non-Sterling-denominated risk-weighted assets.

Equity risk

Equity risk arises primarily from three different sources:

• The Group's private equity exposure from investments held by Lloyds Development Capital and its stake in BGF, both within the Equities sub-group

• A small number of legacy strategic equity holdings, for example Visa Inc Preference Shares, and recent minority fintech stakes, all held in the Equities sub-group

• A small exposure to Lloyds Banking Group share price through deferred shares and deferred options granted to employees as part of their benefits package

Credit spread risk

Credit spread risk arises largely from:

(i) the liquid asset portfolio held in the management of Group liquidity, comprising of government, supranational and other eligible assets;

(ii) the Credit Valuation Adjustment (CVA) and Debit Valuation Adjustment (DVA) sensitivity to credit spreads;

(iii) a number of the Group’s structured medium-term notes where the Group has elected to fair value the notes through the profit and loss account; and

(iv) banking book assets in Commercial Banking held at fair value under IFRS 9.

MEASUREMENT

Interest rate risk exposure is monitored monthly using, primarily:

Market value sensitivity: this methodology considers all repricing mismatches (behaviourally adjusted where appropriate) in the current balance sheet and calculates the change in market value that would result from an instantaneous 25, 100 and 200 basis points parallel rise or fall in the yield curve. Sterling interest rates are modelled with a floor below zero per cent, with negative rate floors also modelled for non-Sterling currencies where appropriate (product-specific floors apply). The market value sensitivities are calculated on a static balance sheet using principal cash flows excluding interest, commercial margins and other spread components and are therefore discounted at the risk-free rate.

Interest income sensitivity: this measures the impact on future net interest income arising from various economic scenarios. These include instantaneous 25, 100 and 200 basis point parallel shifts in all yield curves and the Group economic scenarios. Sterling interest rates are modelled with a floor below zero per cent, with negative rate floors also modelled for non-Sterling currencies where appropriate (product-specific floors apply). These scenarios are reviewed every year and are designed to replicate severe but plausible economic events, capturing risks that would not be evident through the use of parallel shocks alone such as basis risk and steepening or flattening of the yield curve. Additional negative rate scenarios are also used, where floors are removed, to ensure that this risk is monitored; however, these are not measured against the limit framework for the purposes of risk appetite.

Unlike the market value sensitivities, the interest income sensitivities incorporate additional behavioural assumptions as to how and when individual products would reprice in response to changing rates. Reported sensitivities are not necessarily predictive of future performance as they do not capture additional management actions that would likely be taken in response to an immediate, large, movement in interest rates. These actions could reduce the net interest income sensitivity, help mitigate any adverse impacts or they may result in changes to total income that are not captured in the net interest income.

Structural hedge: the structural hedging programme managing interest rate risk in the banking book relies on assumptions made around customer behaviour. A number of metrics are in place to monitor the risks within the portfolio.

Market risk, important parts from the 2021 Annual Report, Royal Bank of Canada

Market risk is defined to be the impact of market prices upon our financial condition. This includes potential gains or losses due to changes in market determined variables such as interest rates, credit spreads, equity prices, commodity prices, foreign exchange rates and implied volatilities.

Market risk controls – FVTPL positions

As an element of the ERAF, the Board approves our overall market risk constraints. GRM creates and manages the control structure for FVTPL positions which ensures that business is conducted on a basis consistent with Board requirements. The Market and Counterparty Credit Risk function within GRM is responsible for creating and managing the controls and governance procedures that ensure that risk taken is consistent with risk appetite constraints set by the Board. These controls include limits on probabilistic measures of potential loss such as Value-at-Risk, Stressed Value-at-Risk, Incremental Risk Charge and stress tests as defined below:

Value-at-Risk (VaR) is a statistical measure of potential loss for a financial portfolio computed at a given level of confidence and over a defined holding period. We measure VaR at the 99th percentile confidence level for price movements over a one-day holding period using historic simulation of the last two years of equally weighted historic market data.

These calculations are updated daily with current risk positions, with the exception of certain less material positions that are not actively traded and are updated on at least a monthly basis.

Stressed Value-at-Risk (SVaR) is calculated in an identical manner as VaR with the exception that it is computed using a fixed historical one-year period of extreme volatility and its inverse rather than the most recent two-year history. The stress period used is a one-year period covering the market volatility observed during Q2 2020. SVaR is calculated daily for all portfolios, with the exception of certain less material positions that are not actively traded and are updated on at least a monthly basis.

VaR and SVaR are statistical estimates based on historical market data and should be interpreted with knowledge of their limitations, which include the following:

• VaR and SVaR will not be predictive of future losses if the realized market movements differ significantly from the historical periods used to compute them.

• VaR and SVaR project potential losses over a one-day holding period and do not project potential losses for risk positions held over longer time periods.

• VaR and SVaR are measured using positions at close of business and do not include the impact of trading and hedging activity over the course of a day.

We validate our VaR and SVaR measures through a variety of means – including subjecting the models to vetting and validation by a group independent of the model developers and by back-testing the VaR against daily marked-to-market revenue to identify and examine events in which actual outcomes in trading revenue exceed the VaR projections.

Incremental Risk Charge (IRC) captures the risk of losses under default or rating changes for issuers of certain traded fixed income instruments. IRC is measured over a one year horizon at a 99.9% confidence level, and captures different liquidity horizons for instruments and concentrations in issuers under a constant level of risk assumption. Changes in measured risk levels are primarily associated with changes in inventory from the applicable fixed income trading portfolios.

Stress tests – Our market risk stress testing program is used to identify and control risk due to large changes in market prices and rates. We conduct stress testing daily on positions that are marked-to-market. The stress tests simulate both historical and hypothetical events which are severe and long-term in duration. Historical scenarios are taken from actual market events and range in duration up to 90 days. Examples include the Global Pandemic of 2020, Global Financial Crisis of 2008 and the Taper Tantrum of 2013.

Hypothetical scenarios are designed to be forward-looking at potential future market stresses, and are designed to be severe but plausible. We are constantly evaluating and refining these scenarios as market conditions change. Stress results are calculated assuming an instantaneous revaluation of our positions with no management action.

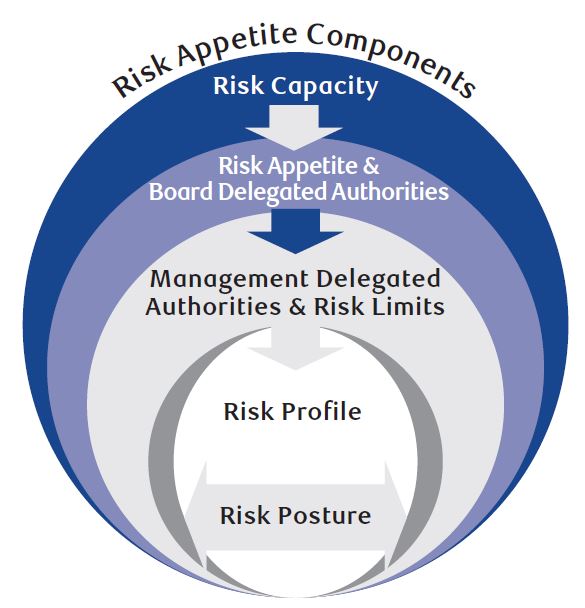

Risk appetite

Effective risk management protects us from unacceptable losses or undesirable outcomes with respect to earnings volatility, capital adequacy or liquidity, reputation risk or other risks while supporting and enabling our overall business strategy. It requires the clear articulation of our risk appetite, which is the amount and type of risk that we are able and willing to accept in the pursuit of our business objectives. It reflects our self-imposed upper bound to risk-taking, set at levels inside of regulatory limits and constraints, and influences our risk management philosophy, Code of Conduct, business practices and resource allocation. It provides clear boundaries and sets an overall tone for balancing risk-reward trade-offs to ensure the long-term viability of the organization.

Our risk appetite is integrated into our strategic, financial, and capital planning processes, as well as ongoing business decision-making processes and is reviewed and approved annually by the Board.

Our Enterprise Risk Appetite Framework (ERAF) outlines the foundational aspects of our approach to risk appetite, articulates our quantitative and qualitative risk appetite statements and their supporting measures and associated constraints, which can be applied at the enterprise, business segment, business unit and legal entity level, and describes our requirements and expectations to embed effective risk appetite practices throughout the organization.

Risk measurement

Quantifying risk is a key component of our enterprise-wide risk and capital management processes. Risk measurement and planning processes are integrated across the enterprise, especially in regards to forward-looking projections and analyses, including but not limited to, stress testing, recovery and resolution planning, and credit provisioning. The degree of integration across our Finance and Risk functions continues to increase in measuring both financial and risk performance.

Certain risks, such as credit, market, liquidity and insurance risks, can be more easily quantified than others, such as operational, reputation, strategic, legal, and regulatory compliance risks. For the risks that are more difficult to quantify, greater emphasis is placed on qualitative risk factors and assessment of activities to gauge the overall level of risk. In addition, judgmental risk measures and techniques such as stress testing, and scenario and sensitivity analyses can be used to assess and measure risks, and we are continuously evolving our risk measures and techniques to manage our risks. Our primary methods for measuring risk include:

• Quantifying expected loss: losses that are statistically expected to occur as a result of conducting business in a given time period;

• Quantifying unexpected loss: an estimate of the deviation of actual earnings from expected earnings, over a specified time horizon;

• Stress testing: evaluates, from a forward looking perspective, the potential effects of a set of specified changes in risk factors, corresponding to exceptional but plausible adverse economic and financial market events; and

• Back-testing: the realized values are compared to the parameter estimates that are currently used in an effort to ensure the parameters remain appropriate for regulatory and economic capital calculations.

Stress testing

Stress testing is an important component of our risk management framework. Stress testing results are used for:

• Assessing the viability of long-term business plans and strategies;

• Monitoring our risk profile relative to our risk appetite in terms of earnings and capital at risk;

• Setting limits;

• Identifying key risks to, and potential shifts in, our capital and liquidity levels, as well as our financial position;

• Enhancing our understanding of available mitigating actions in response to potential adverse events; and

• Assessing the adequacy of our capital and liquidity levels.

Our enterprise-wide stress tests evaluate key balance sheet, income statement, leverage, capital, and liquidity impacts arising from risk exposures and changes in earnings. The results are used by the Board, Group Risk Committee (GRC) and senior management risk committees to understand our performance drivers under stress, and review stressed capital, leverage, and liquidity ratios against regulatory thresholds and internal limits. The results are also incorporated into our Internal Capital Adequacy Assessment Process (ICAAP) and capital plan analyses.

We evaluate a number of enterprise-wide stress scenarios over a multi-year horizon, featuring a range of severities. Our Board reviews the recommended scenarios, and GRM leads the scenario assessment process. Results from across the organization are integrated to develop an enterprise-wide view of the impacts, with input from subject matter experts in GRM, Corporate Treasury, Finance, and Economics. Generally, our stress testing scenarios evaluate global recessions, equity market corrections, elevated debt levels, trade policies, changes in interest rates, real estate price corrections, and shocks to credit spreads and commodity markets, among other factors. During our fiscal 2021 stress testing exercises, we addressed several emerging risks inclusive of further waves of the COVID-19 pandemic, inflation risk as well as physical and transitional climate risk, with a focus on the impacts of these risks on revenue, net income and capital projections.

Ongoing stress testing and scenario analyses within specific risk types, such as market risk (including Interest Rate Risk in the Banking Book (IRRBB)), liquidity risk, retail and wholesale credit risk, operational risk, and insurance risk, supplement and support our enterprise-wide analyses. Results from these risk-specific programs are used in a variety of decision-making processes including risk limit setting, portfolio composition evaluation, risk appetite articulation and business strategy implementation.

In addition to ongoing enterprise-wide and risk specific stress testing programs, we use ad hoc and reverse stress testing to deepen our knowledge of the risks we face. Ad hoc stress tests are one-off analyses used to investigate developing conditions or to stress a particular portfolio in more depth. Reverse stress tests, starting with a severe outcome and aiming to reverseengineer scenarios that might lead to it, are used in risk identification and understanding of risk/return boundaries. In addition to internal stress tests, we participate in a number of regulator-required stress test exercises, on a periodic basis, across several jurisdictions.

Model governance and validation

Quantitative models are used for many purposes including, but not limited to, the valuation of financial products, the identification, measurement and management of different types of risk, stress testing, assessing capital adequacy, informing business and risk decisions, measuring compliance with internal limits, meeting financial reporting and regulatory requirements, and issuing public disclosures.

Model risk is the risk of adverse financial and/or reputational consequences to the enterprise arising from the use or misuse of a model at any stage throughout its life cycle and is managed through our model risk governance and oversight structure. The governance and oversight structure, which is implemented through our three lines of defence governance model, is founded on the basis that model risk management is a shared responsibility across the three lines spanning all stages of the model’s life cycle. We continue to evolve our governance model to take into account any new risk considerations that may emerge from the growing use of Artificial Intelligence (AI) methods and applications in our models across our organization.

Prior to being used, models are subject to an independent validation and approval by our enterprise model risk management function, a team of modelling professionals with reporting lines independent of those of the model owners, developers and users. The validation seeks to ensure that models are sound and capable of fulfilling their intended use. In addition to independently validating models prior to use, our enterprise model risk management function provides controls that span the life-cycle of a model, including model change management procedures, requirements for ongoing monitoring, and annual assessments to ensure each model continues to serve its intended purpose.

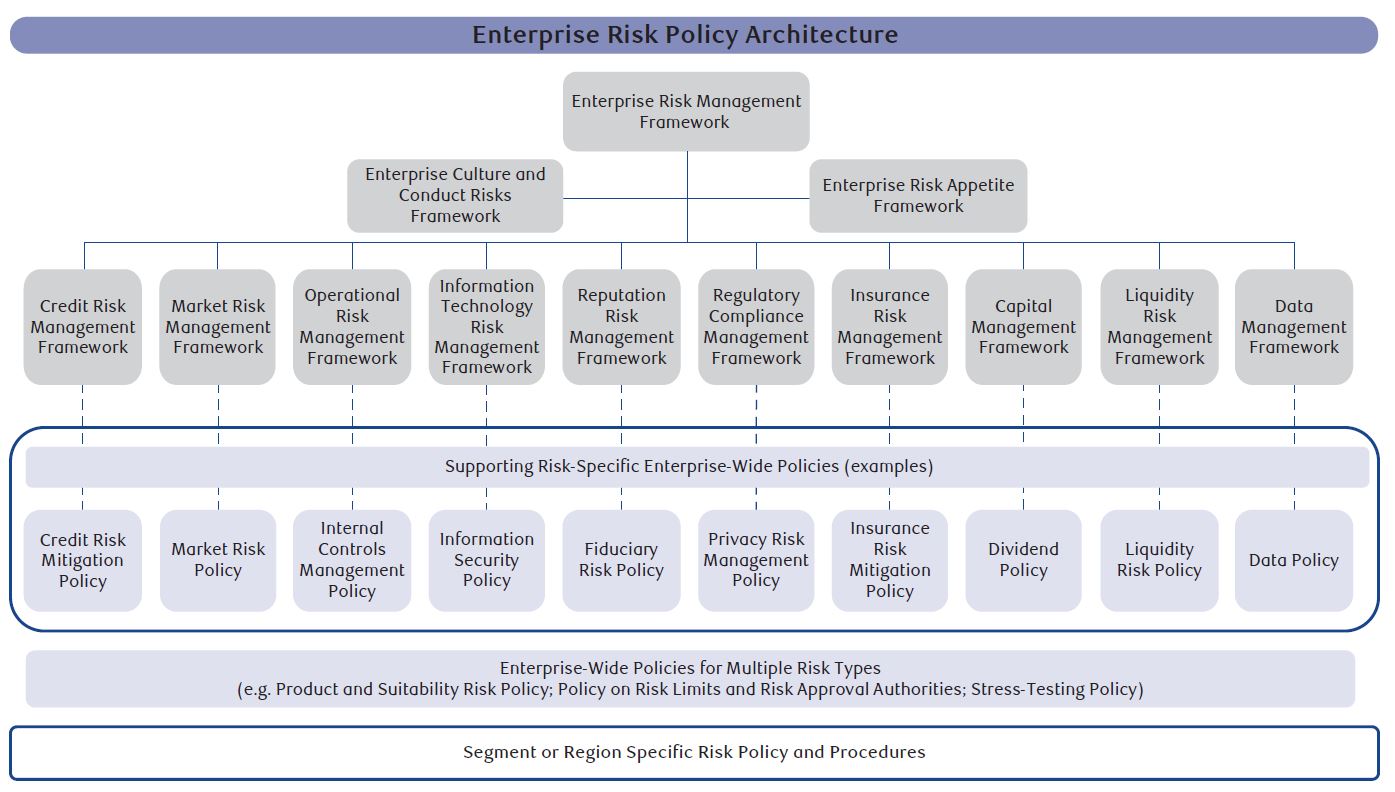

Risk control

Our enterprise-wide risk management approach is supported by a comprehensive set of risk controls that are defined in our ERMF. The ERMF serves as the foundation for our approach to risk management and sets the expectations for the development and communication of policies, the establishment of formal independent risk review and approval processes, and the establishment of delegated authorities and risk limits. The ERMF is further reinforced and supported by a number of additional Board-approved risk frameworks, various policies thereunder and a comprehensive set of risk controls. Together, our risk frameworks and supporting policies provide direction and insight on how respective risks are identified, assessed, measured, managed, mitigated, monitored and reported. The enterprise-wide policies are considered our minimum requirements, articulating the parameters within which business groups and employees must operate.

You may also visit:

The Role of the Risk Officer: https://www.risk-officer.com/Role_Of_Risk_Officer.html

Credit Risk: https://www.risk-officer.com/Credit_Risk.htm

Market Risk: https://www.risk-officer.com/Market_Risk.htm

Operational Risk: https://www.risk-officer.com/Operational_Risk.htm

Systemic Risk: https://www.risk-officer.com/Systemic_Risk.htm

Political Risk: https://www.risk-officer.com/Political_Risk.htm

Strategic Risk: https://www.risk-officer.com/Strategic_Risk.htm

Conduct Risk: https://www.risk-officer.com/Conduct_Risk.htm

Reputation Risk: https://www.risk-officer.com/Reputation_Risk.htm

Liquidity Risk: https://www.risk-officer.com/Liquidity_Risk.htm

Cyber Risk: https://www.risk-officer.com/Cyber_Risk.htm

Climate Risk: https://www.risk-officer.com/Climate_Risk.htm

Emerging Risk: https://www.risk-officer.com/Emerging_Risk.htm

Membership and certification

Become a standard, premium or lifetime member. Get certified.

In the Reading Room (RR) of the association you can find our weekly newsletter - "Top risk and compliance management news stories and world events, that (for better or for worse) shaped the week's agenda, and what is next". Our Reading Room

contact us

Lyn Spooner

Email: lyn@risk-compliance-association.com

George Lekatis

President of the International Association of Risk and Compliance Professionals (IARCP)

1200 G Street NW Suite 800, Washington DC 20005, USA - Tel: (202) 449-9750

Email: lekatis@risk-compliance-association.com