Strategic Risk

What is Strategic Risk?

Strategy is the preparation and planning for success. Strategic decisions reflect management's view of the future. Strategic risk is the risk that the preparation and planning will fail, or will not lead to the results expected.

Strategic risk is the risk to earnings, capital, or liquidity arising from adverse business decisions, improper implementation of strategic initiatives, or inadequate responses to changes in the external operating environment.

In order to develop a strategy, firms and organizations make assessments of future market conditions, supply and demand trends, and future costs and earnings. Strategic risk is the risk that the assessments associated with the markets, shareholders, stakeholders, business partners, customers and suppliers, and the strategic decisions that are based on the assessments are not correct.

The external environment can change significantly for reasons external to each organization. For example, new competitors will emerge, new competing products will be released, or laws and regulations will change. Microsoft entering the computer games market with the X-box console in 2001 is a good exaple of an external strategic risk.

Strategic risk is normally more important than other types of risk and often less well understood and quantified. Strategic risk is complex and difficult to model, as there are complex and long-term variables that are very difficult to quantify.

Learning from the Annual Reports

Strategic Risk, important parts from the 2021 Annual Report, Lloyds Banking Group plc

DEFINITION

Strategic risk is defined as the risk which results from:

• Incorrect assumptions about internal or external operating environments

• Failure to understand the potential impact of strategic responses and business plans on existing risk types

• Failure to respond or the inappropriate strategic response to material changes in the external or internal operating environments

EXPOSURES

The Group faces significant risks due to the changing regulatory and competitive environments in the financial services sector, with an increased pace, scale and complexity of change. Customer, shareholder and employee expectations continue to evolve and current societal trends are being accelerated following the COVID-19 pandemic.

Strategic risks can manifest themselves in existing principal risks or as new exposures which could adversely impact the Group and its businesses.

In considering strategic risks, a key focus is the interconnectivity of individual risks and the cumulative effect of different risks on the Group’s overall risk profile.

The Group has invested in implementing a robust framework for the identification, assessment and quantification of strategic risks and their incorporation into business planning and strategic investment decisions. With Board support, the Group will continue to invest in evolving the strategic risk management framework and embedding it into the Group's day-to-day business operations.

MEASUREMENT

The Group assesses and monitors strategic risk implications as part of business planning and in its day-to-day activities, ensuring they respond appropriately to internal and external factors including changes to regulatory, macroeconomic and competitive environments. An assessment is made of the key strategic risks that are considered to impact the Group, leveraging internal and external information and the key mitigants or actions that could be taken in response.

2021 saw development of the Group’s quantitative risk assessment approach, assessing the:

• Connectivity of inherent risks, which can magnify their impact and severity

• Time horizons in respect of the crystallisation of impacts, should risks manifest

MITIGATION

The range of mitigating actions includes the following:

• Horizon scanning is conducted across the Group to identify potential threats, risks, emerging issues and opportunities and to explore future trends

• The Group’s business planning processes include formal assessment of the strategic risk implications of new business, product entries and other strategic initiatives

• The Group’s governance framework mandates individuals' and committees' responsibilities and decision-making rights, to ensure that strategic risks are appropriately reported and escalated

MONITORING

A review of the Group’s strategic risks is undertaken on an annual basis and the findings are reported to the Group and Board Risk Committees.

Risks, alongside their control effectiveness, are articulated and reported regularly to Group and Board Risk Committees.

Strategic risk is a significant source of risk for the Group, influencing the Group’s strategy, business model, performance and risk profile.

Significant work has been undertaken during 2021 to understand the risk implications of the Group’s strategy and the key drivers of strategic risk.

Key mitigating actions:

• Considering the strategic implications of emerging trends and addressing them through our strategy

• Integration of strategic risk into business planning process and embedding into day-to-day risk management

Strategic risk themes

Understanding the potential risk implications of our strategy is an important area of focus. Using both quantitative and qualitative analysis, key strategic risk themes have been identified and assessed (see below). These risks are aligned to the key areas of focus in the Group’s strategy and can result on impacts in the Group’s wider principal risks.

Organisational purpose: An organisational purpose with clear underlying principles and mission statements will enable us to build a more profitable and sustainable business for the Group’s stakeholders. Risks may arise from:

• Conflicting interpretation of the key principles and mission statement

• Inability to inspire the culture and galvanise the organisation to support a progressive strategy

• Stated purpose failing to resonate with our stakeholders due to conflicting objectives

Customer proposition: Risk of adverse impacts on reputation, customer attraction, customer retention and income generation, arising from:

• Inappropriate products and services

• Inability to respond to changing customer profiles and needs

• Failure to maintain trust and deepen relationships

Talent attraction and retention: Inability to meet the Group’s customer, colleague and transformation goals due to:

• Competition for specialist skills in a challenging labour market

• Failure to attract, develop and retain talent and capabilities for delivering the Group’s agenda

Climate change: Failure to:

• Adapt to shifting consumer and colleague expectations

• Achieve regulatory and external climate commitments

• Support the transition to a low carbon economy as both a lender and employer

Technology advances: Potential for greater operational costs, reduced resilience and uncompetitive or inappropriate customer offering, driven by:

• Failure to keep pace with advances in technology

• Inability to effectively leverage data, while ensuring strong data ethics

• Misalignment of technology versus customer appetite

Strategic Risk, important parts from the 2021 Annual Report, Citigroup Inc.

Strategic risk is the risk of a sustained impact (not episodic impact) to Citi’s core strategic objectives as measured by impacts on anticipated earnings, market capitalization, or capital, arising from the external factors affecting the Company’s operating environment; as well as the risks associated with defining the strategy and executing the strategy, which are identified, measured and managed as part of the Strategic Risk Framework at the Enterprise Level.

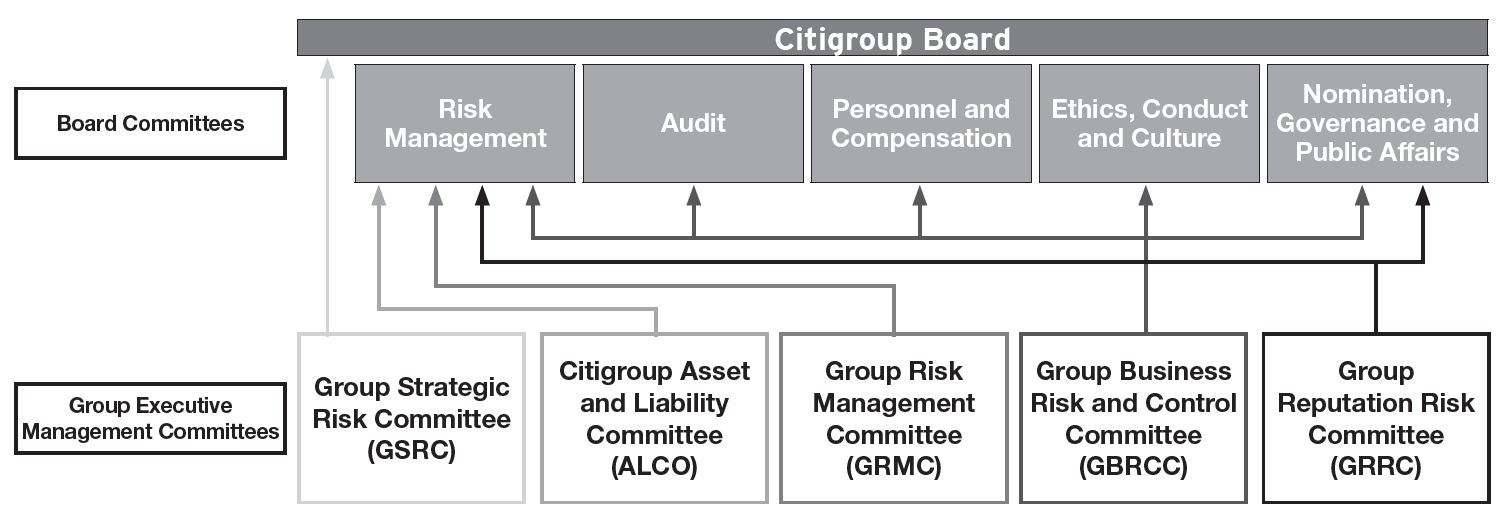

The Group Strategic Risk Committee (GSRC) provides governance oversight of Citi’s management actions to adequately identify, monitor, report, manage and escalate all material strategic risks facing Citi.

Risk Factors, Strategic Risk

Rapidly Evolving Challenges and Uncertainties Related to the COVID-19 Pandemic in the U.S. and Globally Will Likely Continue to Have Negative Impacts on Citi’s Businesses and Results of Operations and Financial Condition.

The COVID-19 pandemic has affected all of the countries and jurisdictions in which Citi operates, including severely impacting global health, financial markets, consumer and business spending and economic conditions.

The extent of the future pandemic impacts remain uncertain and will likely evolve by region, country or state, largely depending on the duration and severity of the public health consequences, including the duration and further spread of the coronavirus as well as any variants becoming more prevalent and impactful; further production, distribution, acceptance and effectiveness of vaccines; availability and efficiency of testing; the public response; and government actions.

The future impacts to global economic conditions may include, among others:

• further disruption of global supply chains;

• higher inflation;

• higher interest rates;

• significant disruption and volatility in financial markets;

• additional closures, reduced activity and failures of many businesses, leading to loss of revenues and net losses;

• further institution of social distancing and restrictions on businesses and the movement of the public in and among the U.S. and other countries; and

• reduced U.S. and global economic output.

The pandemic has had, and may continue to have, negative impacts on Citi’s businesses and overall results of operations and financial condition, which could be material.

The extent of the impact on Citi’s operations and financial performance, including its ability to execute its business strategies and initiatives, will continue to depend significantly on future developments in the U.S. and globally.

Such developments are uncertain and cannot be predicted, including the course of the coronavirus, as well as any weakness or slowing in the economic recovery or a further economic downturn, whether due to further supply chain disruptions, inflation trends, higher interest rates or otherwise.

The pandemic may not be sufficiently contained for an extended period of time. A prolonged health crisis could reduce economic activity in the U.S. and other countries, resulting in additional declines or weakness in employment trends and business and consumer confidence.

These factors could negatively impact global economic activity and markets; cause a continued decline in the demand for Citi’s products and services and in its revenues; further increase Citi’s credit and other costs; and may result in impairment of long-lived assets or goodwill.

These factors could also cause an increase in Citi’s balance sheet, risk-weighted assets and ACL, resulting in a decline in regulatory capital ratios or liquidity measures, as well as regulatory demands for higher capital levels and/or limitations or reductions in capital distributions (such as common share repurchases and dividends). Moreover, any disruption or failure of Citi’s performance of, or its ability to perform, key business functions, as a result of the continued spread of COVID-19 or otherwise, could adversely affect Citi’s operations.

The impact of the pandemic on Citi’s consumer and corporate borrowers will vary by sector or industry, with some borrowers experiencing greater stress levels, particularly as credit and customer assistance support further winds down, which could lead to increased pressure on their results of operations and financial condition, increased borrowings or credit ratings downgrades, thus likely leading to higher credit costs for Citi.

These borrowers include, among others, businesses that are more directly impacted by the institution of social distancing, the movement of the public and store closures. In addition, stress levels ultimately experienced by Citi’s borrowers may be different from and more intense than assumptions made in prior estimates or models used by Citi, resulting in an increase in Citi’s ACL or net credit losses, particularly as the benefits of fiscal stimulus and government support programs diminish.

Ongoing legislative and regulatory changes in the U.S. and globally to address the economic impact from the pandemic could further affect Citi’s businesses, operations and financial performance. Citi could also face challenges, including legal and reputational, and scrutiny in its efforts to provide relief measures.

Such efforts have resulted in, and may continue to result in, litigation, including class actions, and regulatory and government actions and proceedings. Such actions may result in judgments, settlements, penalties and fines adverse to Citi. In addition, the different types of government actions could vary in scale and duration across jurisdictions and regions with varying degrees of effectiveness.

Citi has taken measures to maintain the health and safety of its colleagues; however, these measures could result in additional expenses, and illness of employees could negatively affect staffing for a period of time. In addition, Citi’s ability to recruit, hire and onboard colleagues in key areas could be negatively impacted by pandemic restrictions as well as Citi’s COVID-19 vaccination requirement (see the qualified colleagues risk factor below).

Further, it is unclear how the macroeconomic or business environment or societal norms may be impacted after the pandemic. The post-pandemic environment may undergo unexpected developments or changes in financial markets, fiscal, monetary, tax and regulatory environments and consumer customer and corporate client behavior.

These developments and changes could have an adverse impact on Citi’s results of operations and financial condition. Ongoing business and regulatory uncertainties and changes may make Citi’s longer-term business, balance sheet and strategic and budget planning more difficult or costly. Citi and its management and businesses may also experience increased or different competitive and other challenges in this environment. To the extent that it is not able to adapt or compete effectively, Citi could experience loss of business and its results of operations and financial condition could suffer (see the competitive challenges risk factor below).

You may also visit:

The Role of the Risk Officer: https://www.risk-officer.com/Role_Of_Risk_Officer.html

Credit Risk: https://www.risk-officer.com/Credit_Risk.htm

Market Risk: https://www.risk-officer.com/Market_Risk.htm

Operational Risk: https://www.risk-officer.com/Operational_Risk.htm

Systemic Risk: https://www.risk-officer.com/Systemic_Risk.htm

Political Risk: https://www.risk-officer.com/Political_Risk.htm

Strategic Risk: https://www.risk-officer.com/Strategic_Risk.htm

Conduct Risk: https://www.risk-officer.com/Conduct_Risk.htm

Reputation Risk: https://www.risk-officer.com/Reputation_Risk.htm

Liquidity Risk: https://www.risk-officer.com/Liquidity_Risk.htm

Cyber Risk: https://www.risk-officer.com/Cyber_Risk.htm

Climate Risk: https://www.risk-officer.com/Climate_Risk.htm

Emerging Risk: https://www.risk-officer.com/Emerging_Risk.htm

Membership and certification

Become a standard, premium or lifetime member. Get certified.

In the Reading Room (RR) of the association you can find our weekly newsletter - "Top risk and compliance management news stories and world events, that (for better or for worse) shaped the week's agenda, and what is next". Our Reading Room

contact us

Lyn Spooner

Email: lyn@risk-compliance-association.com

George Lekatis

President of the International Association of Risk and Compliance Professionals (IARCP)

1200 G Street NW Suite 800, Washington DC 20005, USA - Tel: (202) 449-9750

Email: lekatis@risk-compliance-association.com