Systemic Risk

What is Systemic Risk?

Systemic risk is the risk of losses in an entire system, as opposed to breakdowns in individual parts of a system, due to interlinkages and interdependencies in the system. The failure of a single entity or cluster of entities can cause a cascading failure, which could affect the entire system.

We can also define systemic risk as the risk that cumulative losses will occur from an event that ignites a series of successive losses along a chain of institutions or markets.

A default by one market participant can have repercussions on other participants, due to the interlocking nature of the financial markets. For example, the default of A in market X, can affect intermediary B’s ability to fulfill its obligations in Markets Y and Z.

Before the global financial crisis, financial stability was mainly considered from a microprudential perspective. Supervisors tried to reduce the risk that individual institutions could fail, without any explicit regard for their impact on the financial system as a whole or on the overall economy.

After the Lehman Brothers’ default, it was obvious that financial stability has a macroprudential or systemic dimension that cannot be ignored.

Macroprudential policies are designed to identify and mitigate risks to systemic stability, in turn reducing the cost to the economy from a disruption in financial services that underpin the workings of financial markets - such as the provision of credit, but also of insurance and payment and settlement services.

Systemic risk and macroprudential policy in insurance, from the European Insurance and Occupational Pensions Authority

The financial crisis has shown the need to further consider the way in which systemic risk is created and/ or amplified, as well as the need to have proper policies in place to address those risks.

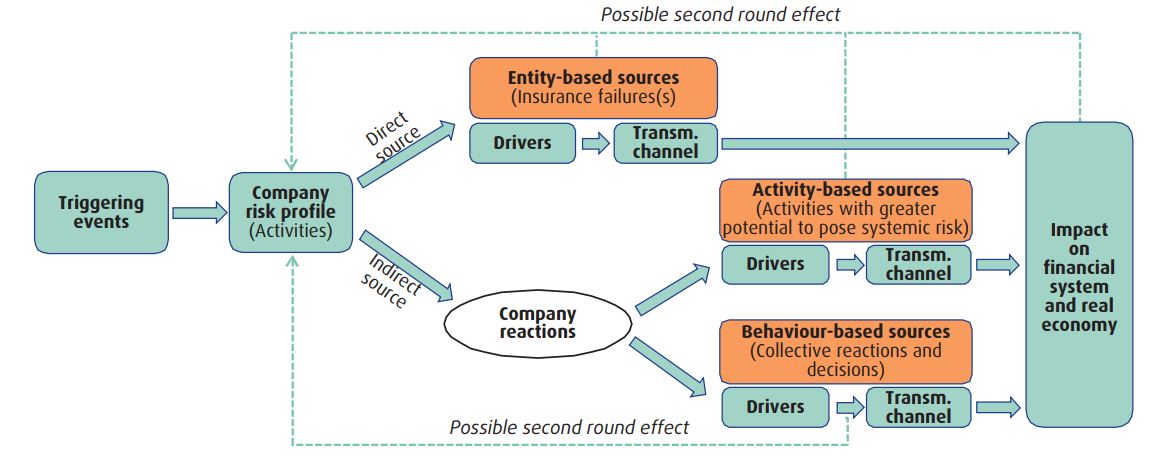

Systemic events could be generated in two ways.

i. The ‘direct’ effect, originated by the failure of a systemically relevant insurer or the collective failure of several insurers generating a cascade effect. This systemic source is defined as ‘entity-based’.

ii. The ‘indirect’ effect, in which possible externalities are enhanced by engagement in potentially systemic activities (activity-based sources) or the widespread common reactions of insurers to exogenous shocks (behaviour-based source).

Potential externalities generated via direct and indirect sources are transferred to the rest of the financial system and to the real economy via specific channels (i.e. the transmission channel) and could induce changes in the risk profile of insurers, eventually generating potential second-round effects.

Main lessons learned from the crisis and status of discussions in insurance

• Microprudential policy should be supplemented with a macroprudential approach. Potential conflicts between the two approaches should be avoided to the extent possible.

• Sources of systemic risk need to be identified.

• A sound macroprudential strategy that links objectives and instruments should be in place. Sufficient macroprudential tools need to be available.

• New macroprudential tools have been introduced to properly address systemic risk.

• The entity-based approach initially developed should be supplemented with an activity-based approach.

• Macroprudential policy may require supranational coordination.

• Macroprudential policies pose several challenges that need due consideration. Overall, macroprudential policy seems to contribute effectively to the mitigation of systemic risk.

Definitions

• Financial stability and systemic risk are two strongly related concepts. Financial stability can be defined as a state whereby the build-up of systemic risk is prevented.

• Systemic risk means a risk of disruption in the financial system with the potential to have serious negative consequences for the internal market and the real economy.

• Macroprudential policy should be understood as a framework that aims at mitigating systemic risk (or the build-up thereof), thereby contributing to the ultimate objective of the stability of the financial system and, as a result, the broader implications for economic growth.

• Macroprudential instruments are qualitative or quantitative tools or measures with system-wide impact that relevant competent authorities (i.e. authorities in charge of preserving the stability of the financial system) put in place with the aim of achieving financial stability.

The macroprudential policy approach contributes to the stability of the financial system — together with other policies (e.g. monetary and fiscal) as well as with microprudential policies. Whereas microprudential policies primarily focus on individual entities, the macroprudential approach focuses on the financial system as a whole.

Relevant lessons learned from the financial crisis and the banking sector

The 2007-2008 financial crisis highlighted the need of a new set of policies aimed at avoiding contagion and contributing to financial stability.

Most of the initiatives developed in the aftermath of this crisis are targeted to the banking sector, which was at the epicentre of the financial crisis. Although the insurance sector differs substantially from the banking sector, some of the lessons from the banking experience could also be useful for insurance.

Microprudential policy should be supplemented with a macroprudential approach. The recent financial crisis revealed that financial regulation and supervision based on microprudential perspective is not always sufficient and cannot work in isolation in order to safeguard financial stability. Therefore, a macroprudential framework is needed to supplement the microprudential one.

For example, according to Crocket (2000), financial stability can be most productively achieved if a better ‘marriage between the microprudential and the macroprudential dimensions’ is achieved. Along these lines, the thesis of Borio (2003) is that the prevention of financial instability can only be improved if the macroprudential approach of the regulatory and supervisory frameworks is strengthened. Many other economists and policymakers have also supported these views.

Indeed, financial stability does not depend solely on the soundness of the individual components that make up the financial system; it also depends on complex interactions and interdependencies between these components, with the possibility for individually sound financial institutions to create imbalances within the economy through their collective activities in some circumstances (for example, rapid lending to certain sectors of the economy could be a source of price bubbles).

Therefore, it became obvious that there can be risks that are not necessarily covered by microprudential policy measures. Contradictions between the micro and the macro spheres should be avoided to the extent possible and convergence should be sought.

Microprudential and macroprudential policies may use similar tools, but with different aims. As a result of this, a potential contradiction may arise.

As explained by Osiński et al. (2013), microprudential and macroprudential policies need to cohabit and conflicts need to be reduced. If not properly addressed, tensions between both approaches will arise, reducing their effectiveness. It follows that there is a risk of diverging interests between the micro and macro approaches that will have to be reconciled.

The sources of systemic risk need to be identified. Macroprudential policies aim to address both the evolution of system-wide risk over time (‘time dimension’) as well as the distribution of risk in the financial system at a given point in time (‘crosssectional dimension’) (BIS, FSB, IMF, 2011).

Examples of it are significant concentrations in certain banking activities (for example concentrations in lending to real estate sector in certain countries), substantial leverages, very rapid lending growth, overreliance on external ratings, high sovereign exposures or mismatching of assets and liabilities.

All these risks and any other potential new challenges need to be timely identified and monitored, and respective mitigating tools and instruments should be implemented both on respective macro and microprudential levels.

A sound macroprudential strategy that links objectives and instruments should be in place. For example, for the banking sector, the ESRB has developed a comprehensive approach which links intermediate objectives, indicators and instruments that should achieve the ultimate objective of financial stability.

The four relevant intermediate objectives aim at preventing/ mitigating systemic risks to financial stability arising from:

(i) an excessive credit growth and leverage,

(ii) an excessive maturity mismatch and market liquidity,

(iii) direct and indirect exposure concentrations and

(iv) misaligned incentives and moral hazard.

Sufficient macroprudential tools need to be available. In 1952, Jan Tinbergen formulated his famous rule, stressing that in order to achieve the economic policy objectives, authorities needed to have instruments that equal in number the objectives.

The financial crisis revealed that either no appropriate tools existed or microprudential measures were used for addressing identified system-wide risks, which were not successful or sufficient.

Lim et al. (2011) consider that tackling one specific risk by combining multiple instruments has the advantages of addressing it from different angles, reduces the scope for circumvention and increases the effectiveness.

New macroprudential tools were introduced to properly address systemic risk. The financial crisis has shown the previous ‘soft communication mechanism’ of macroprudential policy occurring mainly through publications of Financial Stability Reports to be inadequate. Therefore, new or revised macroprudential instruments were introduced in several countries such as capital surcharges on excessive risk concentrations or countercyclical risks, and/or for systemically important financial institutions at both country and global level.

Other tools include, for example, liquidity ratios, loan-to-value/loan-to-income limits (largely implemented in mortgage lending), leverage ratio, revised, structural measures (e.g. Volcker rule in the US), or recovery and resolution planning.

Reducing Systemic Risk - by Chairman Ben S. Bernanke, at the Federal Reserve Bank of Kansas City's Annual Economic Symposium

The regulation and supervisory oversight of financial institutions is another critical tool for limiting systemic risk. In general, effective government oversight of individual institutions increases financial resilience and reduces moral hazard by attempting to ensure that all financial firms with access to some sort of federal safety net‑‑including those that creditors may believe are too big to fail--maintain adequate buffers of capital and liquidity and develop comprehensive approaches to risk and liquidity management. Importantly, a well-designed supervisory regime complements rather than supplants market discipline. Indeed, regulation can serve to strengthen market discipline, for example, by mandating a transparent disclosure regime for financial firms.

Going forward, a critical question for regulators and supervisors is what their appropriate "field of vision" should be. Under our current system of safety-and-soundness regulation, supervisors often focus on the financial conditions of individual institutions in isolation. An alternative approach, which has been called systemwide or macroprudential oversight, would broaden the mandate of regulators and supervisors to encompass consideration of potential systemic risks and weaknesses as well.

At least informally, financial regulation and supervision in the United States already include some macroprudential elements. As one illustration, many of the supervisory guidances issued by federal bank regulators have been motivated, at least in part, by concerns that a particular industry trend posed risks to the stability of the banking system as a whole, not just to individual institutions. For example, following lengthy comment periods, in 2006, the federal banking supervisors issued formal guidance on underwriting and managing the risks of nontraditional mortgages, such as interest-only and negative amortization mortgages, as well as guidance warning banks against excessive concentrations in commercial real estate lending.

These guidances likely would not have been issued if the federal regulators had viewed the issues they addressed as being isolated to a few banks. The regulators were concerned not only about individual banks but also about the systemic risks associated with excessive industry-wide concentrations (of commercial real estate or nontraditional mortgages) or an industry-wide pattern of certain practices (for example, in underwriting exotic mortgages). Note that, in warning against excessive concentrations or common exposures across the banking system, regulators need not make a judgment about whether a particular asset class is mispriced--although rapid changes in asset prices or risk premiums may increase the level of concern. Rather, their task is to determine the risks imposed on the system as a whole if common exposures significantly increase the correlation of returns across institutions.

The development of supervisory guidances is a process which often involves soliciting comments from the industry and the public and, where applicable, developing a consensus among the banking regulators. In that respect, the process is not always as nimble as we might like. For that reason, less-formal processes may sometimes be more effective and timely. As a case in point, the Federal Reserve--in close cooperation with other domestic and foreign regulators--regularly conducts so-called horizontal reviews of large financial institutions, focused on specific issues and practices. Recent reviews have considered topics such as leveraged loans, enterprise-wide risk management, and liquidity practices.

The lessons learned from these reviews are shared with both the institutions participating in these reviews as well as other institutions for which the information might be beneficial. Like supervisory guidance, these reviews help increase the safety and soundness of individual institutions but they may also identify common weaknesses and risks that may have implications for broader systemic stability. In my view, making the systemic risk rationale for guidances and reviews more explicit is certainly feasible and would be a useful step toward a more systemic orientation for financial regulation and supervision.

A systemwide focus for financial regulation would also increase attention to how the incentives and constraints created by regulations affect behavior, especially risk-taking, through the credit cycle. During a period of economic weakness, for example, a prudential supervisor concerned only with the safety and soundness of a particular institution will tend to push for very conservative lending policies. In contrast, the macroprudential supervisor would recognize that, for the system as a whole, excessively conservative lending policies could prove counterproductive if they contribute to a weaker economic and credit environment.Similarly, risk concentrations that might be acceptable at a single institution in a period of economic expansion could be dangerous if they existed at a large number of institutions simultaneously. I do not have the time today to do justice to the question of the procyclicality of, say, capital regulations and accounting rules. This topic has received a great deal of attention elsewhere and has also engaged the attention of regulators; in particular, the framers of the Basel II capital accord have made significant efforts to measure regulatory capital needs "through the cycle" to mitigate procyclicality. However, as we consider ways to strengthen the system for the future in light of what we have learned over the past year, we should critically examine capital regulations, provisioning policies, and other rules applied to financial institutions to determine whether, collectively, they increase the procyclicality of credit extension beyond the point that is best for the system as a whole.

A yet more ambitious approach to macroprudential regulation would involve an attempt by regulators to develop a more fully integrated overview of the entire financial system. In principle, such an approach would appear well justified, as our financial system has become less bank-centered and because activities or risk-taking not permitted to regulated institutions have a way of migrating to other financial firms or markets. Some caution is in order, however, as this more comprehensive approach would be technically demanding and possibly very costly both for the regulators and the firms they supervise.

It would likely require at least periodic surveillance and information-gathering from a wide range of nonbank institutions. Increased coordination would be required among the private- and public-sector supervisors of exchanges and other financial markets to keep up to date with evolving practices and products and to try to identify those which may pose risks outside the purview of each individual regulator. International regulatory coordination, already quite extensive, would need to be expanded further.

One might imagine also conducting formal stress tests, not at the firm level as occurs now, but for a range of firms and markets simultaneously. Doing so might reveal important interactions that are missed by stress tests at the level of the individual firm. For example, such an exercise might suggest that a sharp change in asset prices would not only affect the value of a particular firm's holdings but also impair liquidity in key markets, with adverse consequences for the ability of the firm to adjust its risk positions or obtain funding.

Systemwide stress tests might also highlight common exposures and "crowded trades" that would not be visible in tests confined to one firm. Again, however, we should not underestimate the technical and information requirements of conducting such exercises effectively. Financial markets move swiftly, firms' holdings and exposures change every day, and financial transactions do not respect national boundaries. Thus, the information requirements for conducting truly comprehensive macroprudential surveillance could be daunting indeed.

Macroprudential supervision also presents communication issues. For example, the expectations of the public and of financial market participants would have to be managed carefully, as such an approach would never eliminate financial crises entirely. Indeed, an expectation by financial market participants that financial crises will never occur would create its own form of moral hazard and encourage behavior that would make financial crises more, rather than less, likely.

With all these caveats, I believe that an increased focus on systemwide risks by regulators and supervisors is inevitable and desirable. However, as we proceed in that direction, we would be wise to maintain a realistic appreciation of the difficulties of comprehensive oversight in a financial system as large, diverse, and globalized as ours.

Although we at the Federal Reserve remain focused on addressing the current risks to economic and financial stability, we have also begun thinking about the lessons for the future. I have discussed today two strategies for reducing systemic risk: strengthening the financial infrastructure, broadly construed, and increasing the systemwide focus of financial regulation and supervision. Work on the financial infrastructure is already well under way, and I expect further progress as the public and private sectors cooperate to address common concerns. The adoption of a regulatory and supervisory approach with a heavier macroprudential focus has a strong rationale, but we should be careful about over-promising, as we are still rather far from having the capacity to implement such an approach in a thoroughgoing way. The Federal Reserve will continue to work with the Congress, other regulators, and the private sector to explore this and other strategies to increase financial stability.

Learning from the Annual Reports

Systemic risk, important parts from the 2021 Annual Report, Royal Bank of Canada

Systemic risk

Systemic risk is the risk that the financial system as a whole, or a major part of it – either in an individual country, a region, or globally – is put in real and immediate danger of collapse or serious damage due to an unforeseen event causing a substantive shock to the financial system with the likelihood of material damage to the economy, and which would result in financial, reputation, legal or other risks for us.

Systemic risk is considered to be the least controllable risk facing us, leading to increased vulnerabilities as experienced during the 2008 global financial crisis and the COVID-19 pandemic. Our ability to mitigate systemic risk when undertaking business activities is limited, other than through collaborative mechanisms between key industry participants, and, as appropriate, the public sector and regulators to reduce the frequency and impact of these risks. The two most significant measures in mitigating the impact of systemic risk are diversification and stress testing.

Our diversified business model, portfolios, products, activities and funding sources help mitigate the potential impacts from systemic risk as well as having established risk limits to ensure our portfolio is diversified, and concentration risk is reduced and remains within our risk appetite.

Stress testing involves consideration of the simultaneous movements in a number of risk factors. It is used to ensure our business strategies and capital planning are robust by measuring the potential impacts of credit, market, liquidity, and operational risks on us, under adverse economic conditions.

Our enterprise-wide stress testing program evaluates the potential effects of a set of specified changes in risk factors, corresponding to exceptional but plausible adverse economic and financial market events. These stress scenarios are evaluated across the organization, and results are integrated to develop an enterprise-wide view of the impacts on our financial results and capital requirements. For further details on our stress testing, refer to the Enterprise risk management section.

Our financial results are affected by the business and economic conditions in the geographic regions in which we operate. These conditions include consumer saving and spending habits as well as consumer borrowing and repayment patterns, business investment, government spending, exchange rates, sovereign debt risks, the level of activity and volatility of the capital markets, strength of the economy and inflation. Given the importance of our Canadian and U.S. operations, an economic downturn may largely affect our personal and business lending activities and may result in higher provisions for credit losses.

Deterioration and uncertainty in global capital markets could result in continued high volatility that would impact results in Capital Markets, while in Wealth Management weaker market conditions could lead to lower average fee-based client assets and transaction volumes. In addition, worsening financial and credit market conditions may adversely affect our ability to access capital markets on favourable terms and could negatively affect our liquidity, resulting in increased funding costs and lower transaction volumes in Capital Markets and Investor & Treasury Services.

Our financial results are also sensitive to changes in interest rates. Central banks globally reduced benchmark interest rates in 2020, largely in response to the impact of the COVID-19 pandemic in an effort to provide support to maintain the resilience and stability of the financial systems. With interest rates remaining low throughout 2021, and expected to continue to remain low into fiscal 2022, we could see net interest income continuing to be unfavourably impacted by spread compression across many of our businesses while an increase in interest rates would benefit our businesses. However, a significant increase in interest rates could also adversely impact household balance sheets, leading to credit deterioration which could negatively impact our financial results, particularly in some of our Personal & Commercial Banking and Wealth Management businesses.

Caution regarding forward-looking statements

From time to time, we make written or oral forward-looking statements within the meaning of certain securities laws, including the “safe harbour” provisions of the United States Private Securities Litigation Reform Act of 1995 and any applicable Canadian securities legislation. We may make forward-looking statements in this 2021 Annual Report, in other filings with Canadian regulators or the SEC, in other reports to shareholders, and in other communications.

Forward-looking statements in this document include, but are not limited to, statements relating to our financial performance objectives, vision and strategic goals, climate related goals, the Economic, market, and regulatory review and outlook for Canadian, U.S., European and global economies, the regulatory environment in which we operate, the Strategic priorities and Outlook sections for each of our business segments, the risk environment including our credit risk, market risk, liquidity and funding risk, and the potential continued impacts of the coronavirus (COVID-19) pandemic on our business operations, financial results, condition and objectives and on the global economy and financial market conditions and includes our President and Chief Executive Officer’s statements.

The forward-looking information contained in this document is presented for the purpose of assisting the holders of our securities and financial analysts in understanding our financial position and results of operations as at and for the periods ended on the dates presented, as well as our financial performance objectives, vision and strategic goals, and may not be appropriate for other purposes. Forward-looking statements are typically identified by words such as “believe”, “expect”, “foresee”, “forecast”, “anticipate”, “intend”, “estimate”, “goal”, “plan” and “project” and similar expressions of future or conditional verbs such as “will”, “may”, “should”, “could” or “would”.

By their very nature, forward-looking statements require us to make assumptions and are subject to inherent risks and uncertainties, which give rise to the possibility that our predictions, forecasts, projections, expectations or conclusions will not prove to be accurate, that our assumptions may not be correct and that our financial performance objectives, vision and strategic goals will not be achieved. We caution readers not to place undue reliance on these statements as a number of risk factors could cause our actual results to differ materially from the expectations expressed in such forward-looking statements.

These factors – many of which are beyond our control and the effects of which can be difficult to predict – include: credit, market, liquidity and funding, insurance, operational, regulatory compliance (which could lead to us being subject to various legal and regulatory proceedings, the potential outcome of which could include regulatory restrictions, penalties and fines), strategic, reputation, competitive, legal and regulatory environment, and systemic risks and other risks discussed in the risk sections and Impact of COVID-19 pandemic section of this 2021 Annual Report including business and economic conditions, information technology and cyber risks, environmental and social risk (including climate change), digital disruption and innovation, Canadian housing and household indebtedness, geopolitical uncertainty, privacy, data and third-party related risks, regulatory changes, culture and conduct, the business and economic conditions in the geographic regions in which we operate, the effects of changes in government fiscal, monetary and other policies, tax risk and transparency, and the emergence of widespread health emergencies or public health crises such as pandemics and epidemics, including the COVID-19 pandemic and its impact on the global economy, financial market conditions and our business operations, and financial results, condition and objectives.

In addition, as we work to advance our climate goals, external factors outside of RBC’s reasonable control may act as constraints on their achievement, including varying decarbonization efforts across economies, the need for thoughtful climate policies around the world, more and better data, reasonably supported methodologies, technological advancements, the evolution of consumer behaviour, the challenges of balancing interim emissions goals with an orderly and just transition, and other significant considerations such as legal and regulatory obligations.

We caution that the foregoing list of risk factors is not exhaustive and other factors could also adversely affect our results. When relying on our forwardlooking statements to make decisions with respect to us, investors and others should carefully consider the foregoing factors and other uncertainties and potential events. Material economic assumptions underlying the forward-looking statements contained in this 2021 Annual Report are set out in the Economic, market and regulatory review and outlook section and for each business segment under the Strategic priorities and Outlook headings.

Except as required by law, we do not undertake to update any forward-looking statement, whether written or oral, that may be made from time to time by us or on our behalf.

You may also visit:

The Role of the Risk Officer: https://www.risk-officer.com/Role_Of_Risk_Officer.html

Credit Risk: https://www.risk-officer.com/Credit_Risk.htm

Market Risk: https://www.risk-officer.com/Market_Risk.htm

Operational Risk: https://www.risk-officer.com/Operational_Risk.htm

Systemic Risk: https://www.risk-officer.com/Systemic_Risk.htm

Political Risk: https://www.risk-officer.com/Political_Risk.htm

Strategic Risk: https://www.risk-officer.com/Strategic_Risk.htm

Conduct Risk: https://www.risk-officer.com/Conduct_Risk.htm

Reputation Risk: https://www.risk-officer.com/Reputation_Risk.htm

Liquidity Risk: https://www.risk-officer.com/Liquidity_Risk.htm

Cyber Risk: https://www.risk-officer.com/Cyber_Risk.htm

Climate Risk: https://www.risk-officer.com/Climate_Risk.htm

Emerging Risk: https://www.risk-officer.com/Emerging_Risk.htm

Membership and certification

Become a standard, premium or lifetime member. Get certified.

In the Reading Room (RR) of the association you can find our weekly newsletter - "Top risk and compliance management news stories and world events, that (for better or for worse) shaped the week's agenda, and what is next". Our Reading Room

contact us

Lyn Spooner

Email: lyn@risk-compliance-association.com

George Lekatis

President of the International Association of Risk and Compliance Professionals (IARCP)

1200 G Street NW Suite 800, Washington DC 20005, USA - Tel: (202) 449-9750

Email: lekatis@risk-compliance-association.com